As we analyze the trajectory of insurance losses 2025, it becomes alarmingly clear that we are on the brink of a financial upheaval in the insurance sector. Recent reports indicate global insured losses have skyrocketed to $84 billion in the first half of this year alone, marking a record high since 2011. The 2025 insurance market is grappling with severe storm insurance claims as violent weather events wreak havoc across the globe. From devastating tornadoes to destructive wildfires, weather-related damages are emerging as a significant driver behind these escalating losses. Given the current trends, it is projected that total insurance losses could surpass the staggering $100 billion threshold, illustrating a new market reality for insurers and policymakers alike.

In examining the financial realities surrounding claims within the insurance industry for 2025, we can’t overlook the profound impact of natural disasters and climate change on the economy. As increasing numbers of severe weather events continue to plague communities, the resultant financial repercussions for underwriters only intensify. Insurers now face unprecedented challenges, characterized by significant payouts triggered by wildfires and storm-related damages. Such dramatic shifts underscore an urgent need to rethink conventional assessments and strategies in managing risk. The current atmosphere serves as both a wake-up call and a call to action for the insurance landscape, compelling stakeholders to address and adapt to a rapidly changing environment.

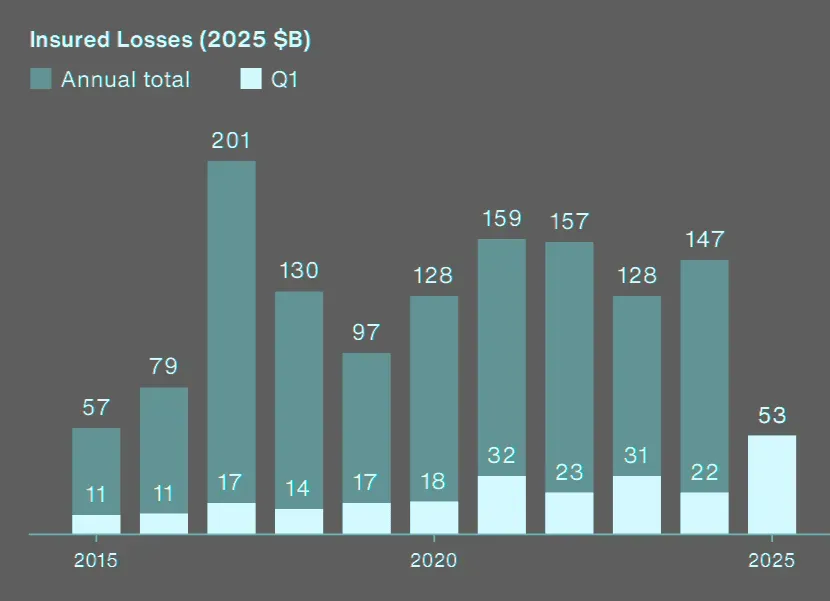

Record Global Insured Losses in 2025

In the first half of 2025, global insured losses surged to an unprecedented $84 billion, marking a significant alarm for the insurance industry. This massive financial toll indicates that insurers are grappling with escalating weather-related damages fueled by climate change. Such losses not only highlight the immediate impact of natural disasters—ranging from severe storms to devastating wildfires—but also signal a shift in the insurance landscape, which is becoming increasingly perilous for carriers and policyholders alike.

Gallagher Re has projected that if these trends continue, total insurance losses for the year could surpass $100 billion, representing a staggering new reality for the 2025 insurance market. This forecast underscores the urgency for insurers to reassess their risk models and pricing strategies in the face of such extreme weather events. The cumulative data suggests that the frequency and severity of weather-related incidents are only set to increase, further straining resources and impacting consumer insurance availability.

The Impact of Severe Storms on Insurance Claims

Severe storms have emerged as a primary contributor to the rising insurance losses in 2025, accounting for over $30 billion in damages during just the first six months. These events, characterized by damaging winds, hail, and lightning, challenge not only the operational capacities of insurance companies but also their financial stability. With 39% of total global insured losses attributed to these violent weather patterns, it is evident that the occurrence of severe storms is significantly altering the risk landscape and the relationship between insurers and their clients.

The financial implications of these storms are profound, particularly in the United States, where eleven storms each resulted in losses exceeding $1 billion. Furthermore, a historic tornado outbreak in March recorded high casualty rates and numerous claims, with estimated insured losses nearing $7.7 billion, solidifying its status as one of the costliest storm events in recent memory. Insurers now face an urgent need for innovative solutions to manage and mitigate risks associated with these increasingly common severe weather conditions.

Wildfire Impact on Insurance Losses

The catastrophic wildfires in California, particularly the Palisades and Eaton wildfires, resulted in devastating insured losses estimated at $40 billion, the highest ever recorded for individual wildfire events. This reality has far-reaching implications for the insurance industry, as it underscores the urgent need for enhanced risk assessment and pricing strategies aimed at wildfire-prone regions. The rising frequency and intensity of wildfires are not only financially burdensome for insurers but also threaten to destabilize the housing market in these high-risk areas.

Furthermore, as people continue to build and live in regions susceptible to wildfires, insurers are compelled to rethink their approach to risk. With soaring costs in materials and labor, even the repairs and replacements of structures can lead to heightened operational costs for insurance providers. The pressing reality is that without fundamental changes in risk management and community planning, insurers may face unsustainable losses, thereby elevating premiums and potentially limiting accessibility for homeowners in vulnerable locations.

Challenges in the 2025 Insurance Market

As we move through 2025, the insurance market is confronted with numerous challenges, significantly influenced by severe weather events and rising costs. Insurers are experiencing an unprecedented increase in claims due to natural disasters, which is straining their financial resources and limiting the availability of affordable coverage. The ultimate goal for insurance companies will be to navigate these challenges while ensuring they can provide necessary protection to their clients without compromising their own stability.

Additionally, rising land and repair costs further complicate the situation, as premiums must reflect the increasing risks and expenses associated with repairing or rebuilding structures. Insurers are under pressure not only to cover claims adequately but also to maintain competitive pricing in a market where losses are climbing to historic levels. Strategic planning and innovative product offerings that address these evolving risks will be essential for navigating the complexities ahead, especially as climate volatility continues to reshape the insurance landscape.

Insurance Strategies for Emerging Weather Threats

In the wake of record-high insured losses in 2025, insurers are seeking innovative strategies to mitigate the impact of emerging weather threats. This involves revising underwriting processes and improving predictive analytics to better assess risk related to severe weather events. By utilizing advanced technology and data analytics, insurers can enhance their understanding of evolving risk factors, allowing them to create more tailored coverage options that reflect the realities of climate change and its influence on severe storms and wildfires.

Moreover, collaboration with communities and regulatory bodies is crucial in developing preventive measures against potential weather-related disasters. Establishing guidelines for construction in high-risk areas and investing in infrastructure resilience can not only benefit policyholders but also help stabilize the insurance market overall. Ultimately, by embracing innovative approaches, insurers can create a sustainable model that addresses the growing threats of weather-related damages while ensuring long-term viability and protection for their clients.

The Economic Implications of Rising Insurance Losses

The economic ramifications of skyrocketing insurance losses in 2025 extend beyond the insurance sector, impacting various industries and consumers alike. As insurers grapple with increased claims from severe weather and the resultant hikes in premiums, the broader economy may experience shifts in consumer spending power and housing market stability. Higher insurance costs can strain household budgets, diminishing disposable income and affecting purchasing behavior in local economies, particularly in regions heavily hit by severe weather.

Additionally, businesses may face higher overhead costs as they adjust to the increased expense of insuring their properties and operations, further affecting their competitiveness. This ripple effect highlights the importance of revisiting policies and approaches to disaster management, as sustainable solutions could serve to mitigate these economic impacts. Solutions could include incentivizing resilience measures or funding community preparedness programs, ultimately fostering a healthier economic landscape amid the adversity of climate-induced insurance losses.

Innovations in Climate Risk Assessment for Insurers

To tackle the challenges of changing climate patterns and emerging severe weather threats, innovative climate risk assessment methodologies are vital for insurers in 2025. Leveraging advanced technologies such as artificial intelligence and machine learning, insurance companies can refine their risk models and develop more accurate predictions of future losses associated with severe storms and wildfires. This type of innovation not only helps insurers select appropriate premiums but also improves their ability to allocate resources more effectively in times of crisis.

Furthermore, expanding access to real-time data regarding weather patterns and regional vulnerabilities can empower insurers to make informed decisions around risk management and claims processing. By enhancing their analytical capabilities, insurers can foster stronger relationships with policyholders through transparent communication about risks and coverage options. Ultimately, this proactive approach to climate risk assessment will be integral to maintaining consumer trust and stability within the increasingly impacted insurance market.

Long-term Solutions to Insurance Market Challenges

In light of unprecedented insured losses and ongoing economic challenges driven by severe weather events, the insurance industry must explore long-term solutions to ensure its sustainability and resilience. Prioritizing strong partnerships between insurers, government agencies, and environmental organizations can lead to collaborative innovation aimed at addressing the underlying causes of rising costs and escalating risks associated with climate change. The combined efforts of multiple stakeholders can result in targeted initiatives that promote better risk management and disaster preparedness.

Additionally, insurers can consider developing new financial products that cater to evolving risks created by climate change. For instance, parametric insurance solutions that provide instant payouts based on predetermined triggers, like specific storm intensity or wildfire behavior, can offer policyholders immediate support when they need it most. Through such innovative products and collaborative strategies, the insurance landscape can adapt to the growing challenges posed by adverse weather conditions while ensuring adequate protection for consumers.

Preparing for Future Insurance Market Trends

As the insurance landscape shifts in response to the growing impact of climate change, preparing for future trends is essential for both insurers and policyholders. The anticipated increase in insurance losses for 2025 serves as a wake-up call for the entire industry to adapt to rapidly altering circumstances. Insurers must stay informed about emerging risks and develop contingency plans that account for potential weather-related challenges, as well as the economic repercussions of rising claims.

Moreover, educating consumers about their risk exposure and encouraging proactive measures—such as reinforcing homes against storms or fires—can significantly lessen future losses. By fostering a culture of preparedness and resilience within communities, insurance companies can help mitigate the impacts of severe weather events while simultaneously building stronger relationships with their policyholders. Emphasizing long-term resilience in both insurance practices and community planning is crucial to create a more sustainable future for all stakeholders in the insurance market.

Frequently Asked Questions

What are the reasons behind the surge in global insured losses in 2025?

In 2025, global insured losses are soaring due to increasingly severe weather-related damages. The first half of the year alone accounted for $84 billion in losses, primarily driven by violent storms, including tornadoes and hail events, which collectively caused significant financial burdens for insurers.

How does the 2025 insurance market reflect changes in wildfire impact on insurance?

The 2025 insurance market is greatly impacted by rising wildfire threats, with events like the Palisades and Eaton wildfires resulting in an estimated $40 billion in insured losses. These unprecedented figures indicate a shift in how insurers must assess risk and pricing in areas prone to wildfires.

What constitutes the majority of insurance losses reported in the first half of 2025?

The majority of the $84 billion in insurance losses in early 2025 is attributed to severe storms, which accounted for 39% of the losses. Specifically, damaging incidents such as hail storms and violent winds have rendered substantial impacts on the insurance sector globally.

Are insurers prepared for the $100 billion threshold in 2025 insurance losses?

Insurers are grappling with the rising likelihood of surpassing the $100 billion threshold in total insurance losses for 2025. Strategies are being reevaluated given the scale of weather-related damages and the increasing frequency of severe storms.

What role do severe storm insurance products play in 2025?

Severe storm insurance products are becoming essential in 2025 as insurers face heightened risks from frequent and severe convective storms. These specialized products aim to provide adequate coverage in light of escalating storm-related damages and losses.

How are rising costs affecting insurance claims in 2025?

Rising costs for materials and labor are driving up the expenses for insurance claims in 2025. This inflationary trend complicates repairs and replacements for properties damaged by severe weather, ultimately increasing the overall insurance losses reported this year.

What trends are visible in weather-related damages that affect insured losses this year?

In 2025, weather-related damages include a notable increase in frequency and severity of storms, alongside the significant impact of wildfires. This trend is shaping the landscape of global insured losses as insurers adapt to the new realities presented by climate change.

How did the storm outbreak from March 2025 influence insurance losses?

The historic storm outbreak from March 13 to March 16, 2025, resulted in over 118 tornado touchdowns across the U.S., leading to projected insured losses nearing $7.7 billion. This event is significant as it ranks among the most expensive severe convective storms in recent history.

What should policyholders know about the implications of increased insurance losses in 2025?

Policyholders need to be aware that increased insurance losses in 2025 could lead to higher premiums and stricter underwriting criteria. Understanding the risks associated with severe weather and wildfires will be crucial for ensuring adequate coverage and financial protection.

What is the expected impact of climate change on future insurance losses?

Climate change is anticipated to exacerbate the occurrence of severe weather events, which will likely result in higher global insured losses in the future. Insurers must adjust their risk models and pricing structures to reflect these evolving patterns in weather-related damages.

| Key Point | Details |

|---|---|

| Global Insured Losses | $84 billion in the first half of 2025, the highest since 2011. |

| Projected Total Losses | Expected to exceed $100 billion by the end of 2025. |

| Impact of Weather Events | Violent storms in the U.S. caused over $30 billion in losses, making up 39% of total losses. |

| Significant Storm Events | Eleven storms in the U.S. caused over $1 billion in losses, with three above $2 billion. |

| Historic Storm Outbreak | March 13-16 storms caused at least 118 tornadoes and an estimated $7.7 billion in insured losses. |

| Wildfire Losses | The Palisades and Eaton wildfires incurred an estimated $40 billion in insured losses. |

| Rising Costs | Increasing material and labor costs are driving up repair and replacement expenses. |

Summary

Insurance losses 2025 are projected to exceed $100 billion, marking a significant increase primarily driven by severe weather events and wildfires. The first half of the year has already seen global insured losses hit $84 billion, highlighting the seriousness of the situation. The ongoing challenges including rising costs related to materials and labor, along with the frequency of damaging storms, solidify the need for insurers and policyholders to prepare for a new market reality in the face of increasing climate-related risks.