Startup funding surge is reshaping the global tech landscape as capital flows more freely to bold founders and scalable ideas. Breaking business news signals not just a headline, but a renewed appetite for innovation and growth across traditional powerhouses and rising hubs, with tech hub funding driving faster rounds. For founders, investors, and policy makers, the current climate offers both opportunities and challenges, from faster rounds to new diligence standards. The headline trend highlights a shift in liquidity toward early-stage and growth-stage startups, with activity expanding beyond marquee centers to include emerging regions. This momentum is shaping expectations for venture capital trends, while fueling seed funding surge and startup investment growth across global ecosystems.

Across the landscape, the discourse shifts to an accelerated cycle of early-stage financing and broader venture activity rather than a single boom. Analysts describe this as a financing boom for startups, driven by sustained VC activity and diversified capital sources. The emphasis on seed rounds and growth-stage investments mirrors a more mature funding environment, with regional dynamics shaping where the money lands. By observing VC funding by region, investors can spot where infrastructure, talent, and commercial traction converge. In plain terms, the era is characterized by more predictable capital, faster diligence, and a widening map of startup ecosystems ready to scale.

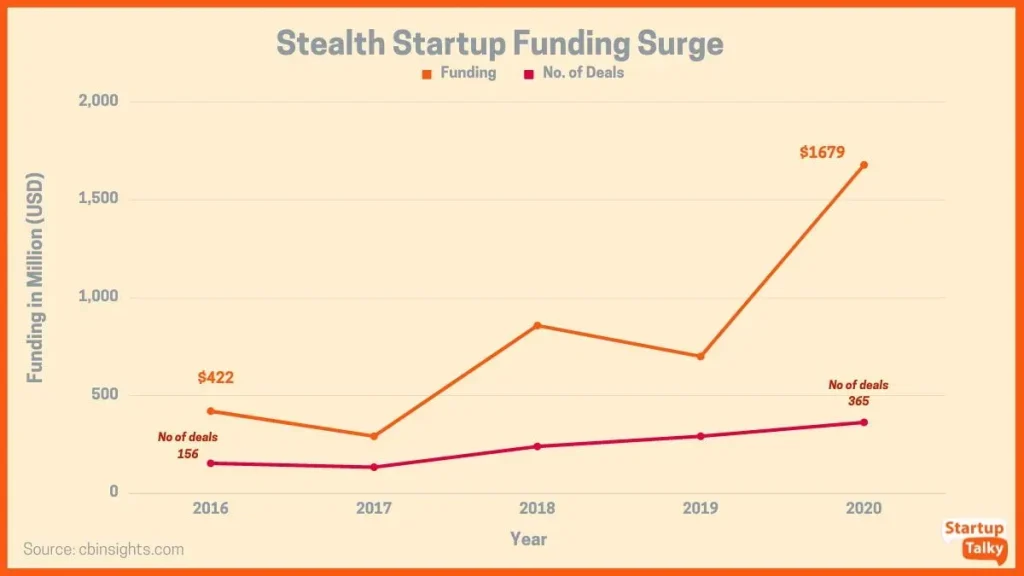

Startup funding surge across global tech hubs drives early-stage momentum

A startup funding surge is reshaping how early-stage ideas scale, with capital flowing into traditional powerhouses and rising stars alike. This shift aligns with evolving venture capital trends that reward capital efficiency, robust unit economics, and tech-enabled product strategies. seed funding surge activity is now widespread, with more frequent rounds and larger checks signaling renewed confidence in product-market fit and rapid iteration. Across diverse tech hubs, startup investment growth is becoming more visible in SaaS, fintech, and health-tech verticals, and tech hub funding is expanding beyond legacy centers thanks to a broader mix of investors and faster due diligence.

Founders and policymakers must navigate the expanding VC funding by region landscape, balancing regional strengths with global go-to-market ambitions. In Silicon Valley, New York, Berlin, and London, capital is chasing deep tech and scalable platforms, while cities like Austin, Madrid, and Singapore attract seed funds and micro funds focused on speed to market and international expansion. The broader pattern—tech hub funding extending to emerging centers—highlights a healthier, more diverse ecosystem and signals that startup investment growth is not limited to traditional markets.

Venture capital trends and regional dynamics fueling startup investment growth

Venture capital trends continue to evolve as LPs seek portfolio resilience and cross-border exposure. The surge in funding has widened the pool of investors from sovereign wealth funds to corporate venture arms, aligning with a broader set of venture capital trends that emphasize strategic value and multi-stage flexibility. Startup investment growth is evident in sectors like AI, cloud infrastructure, cybersecurity, and climate tech, with tech hub funding expanding into secondary markets and regional clusters in Asia Pacific, Europe, and the Americas.

Regional dynamics are shaping deal flow and risk profiles, making VC funding by region more nuanced. Founders should tailor product-market strategies to local regulatory environments while keeping an eye on global scale, partnerships, and exit options. For investors, diversification across regions and sectors remains essential to balancing risk and accessing high-growth opportunities, supported by data-driven diligence and milestone-driven funding milestones.

Frequently Asked Questions

How does the startup funding surge reshape venture capital trends across regions and tech hubs?

The startup funding surge signals a renewed appetite for risk in venture capital trends, with stronger activity in seed rounds and early growth stages. Across North America, Europe, and Asia Pacific, traditional hubs and emerging centers are seeing faster decisions, larger seed checks, and more varied investor participation, including family offices and corporate venture arms. Tech hub funding is expanding beyond coastlines as capital flows to capital-efficient models with clear unit economics. Founders should emphasize scalable plans, defensible technology, and realistic milestones to capitalize on this surge. For investors, this environment highlights the value of regional networks, cross-border opportunities, and diversified portfolios as part of the startup investment growth story.

What should founders consider as the seed funding surge accelerates early-stage rounds in a world of VC funding by region?

During the seed funding surge, founders should prioritize a capital-efficient model and early product-market fit to attract multiple investors. With VC funding by region broadening the pool, diversify sources—seed funds, angel networks, corporate venture arms, and sovereign wealth-backed funds—across the hubs that best match the product. Prepare for expedited due diligence: tidy cap tables, credible unit economics, and transparent traction. Tailor the fundraising approach to regional dynamics, leveraging local partnerships and incentives to accelerate go-to-market. Maintain discipline on burn and milestones so you can move quickly when the right terms appear.

| Topic | Key Points |

|---|---|

| Overview | A notable shift in funding: a startup funding surge across global tech hubs signals renewed appetite for bold ideas and scalable technology. Capital is flowing to early- and growth-stage startups, creating opportunities and challenges for founders, investors, and policy makers. |

| What the surge looks like across hubs | More diverse rounds, quicker decision times; seed and Series A activity returning to normal cadence; larger check sizes; broader mix of investors; activity across mature markets and emerging hubs. |

| Regional hotspots | NA: Silicon Valley, NYC, Austin, Toronto; Europe: Berlin, London, Madrid, Paris, Nordic capitals; APAC: Bengaluru, Singapore, Shanghai; Latin America and Africa growing; sectors include deep tech, SaaS, fintech, health tech, AI, climate tech. |

| Drivers | Renewed risk appetite; AI, cloud, cybersecurity, data analytics demand; returning capital liquidity; diverse investors (family offices, sovereign funds, corporate VC); capital-efficient, product-led founders; cross-border scaling; supportive policy. |

| Seed vs Growth funding | Seed rounds larger/more frequent; growth rounds deployed in tranches; longer rounds tied to milestones; emphasis on product/market fit, unit economics, profitability; ecosystem maturation. |

| Regional breakdown & sector focus | NA: software, fintech, health tech, AI-enabled platforms; Europe: SaaS, cybersecurity, climate tech; APAC: AI, infrastructure software, semiconductors, cloud; emerging markets: mobile-first, logistics, local-market fit; top sectors: AI, SaaS, fintech, climate tech, health tech, digital infrastructure. |

| Implications for founders | Capital-efficient plans, faster funding cycles, favorable terms; competition for mission-driven teams; strong value proposition, GTM, profitability plan; importance of regional ecosystems and policy alignment. |

| Implications for investors | Broader, deeper deal flow; need to differentiate via execution, data-driven risk assessment; robust milestone pipelines; regional collaboration and diversification. |

| What founders can do to capitalize | Build capital-efficient models; focus on traction and milestones; diversify funding sources; prepare for rapid due diligence; leverage regional advantages. |

| Case studies & practical takeaways | Health tech: rapid onboarding and low CAC; AI: clear product-market fit with efficiency gains; climate tech: pilots funded by public/private capital; success comes when product, customers, and capital align. |

| Risks & market realities | Valuation compression risk if growth misses; macro headwinds; disciplined burn; diversified portfolios across regions and sectors. |